Key takeaways

- In the fourth quarter of 2024, global real house prices decreased by 1.6% year on year (yoy), a decline rate similar to the previous quarters; this was despite a modest rise in nominal prices (+1.8%).

- Advanced economies (AEs) saw real house price growth of 1.0% yoy, led by developments in the euro area (+1.9%). In contrast, prices in emerging market economies (EMEs) extended their decline (–3.5%), largely driven by a 5.7% drop in Asia. Developments exhibited even greater variability across individual jurisdictions.

- From a long-term perspective, global real house prices remain 20% above their levels observed after the 2007-09 Great Financial Crisis.

- To access the full data set, visit Residential property prices – overview | BIS Data Portal.

Summary of latest developments

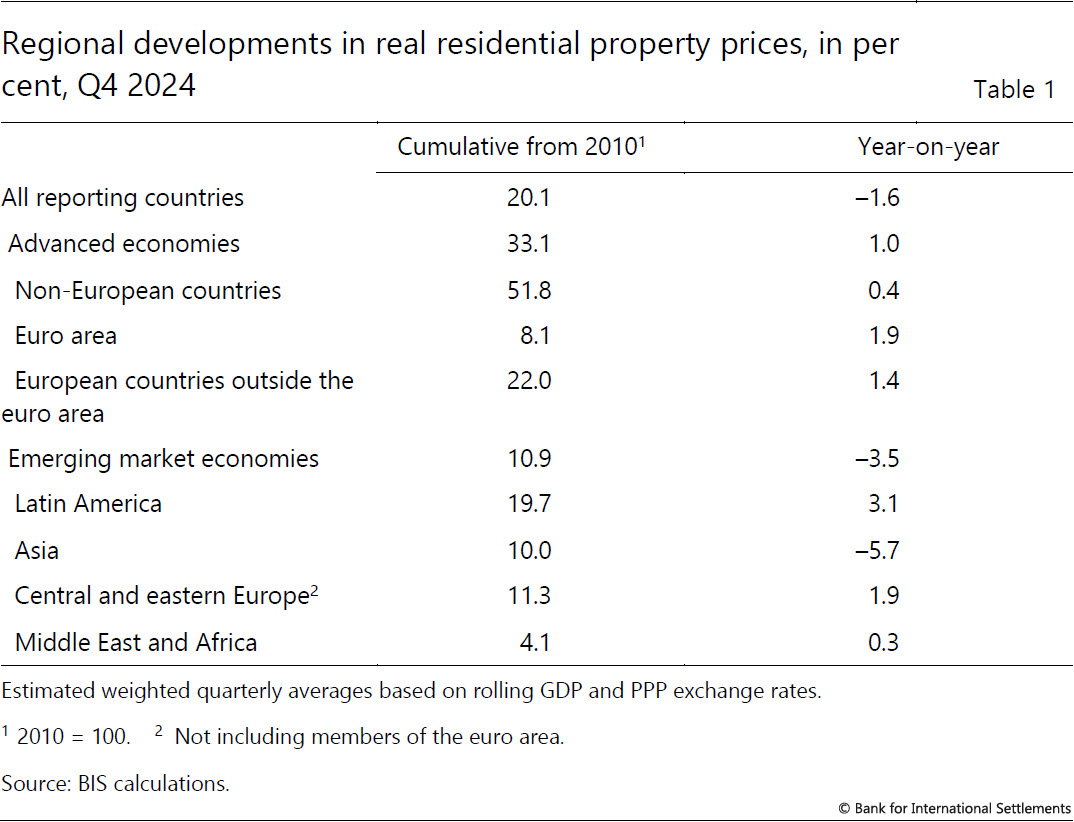

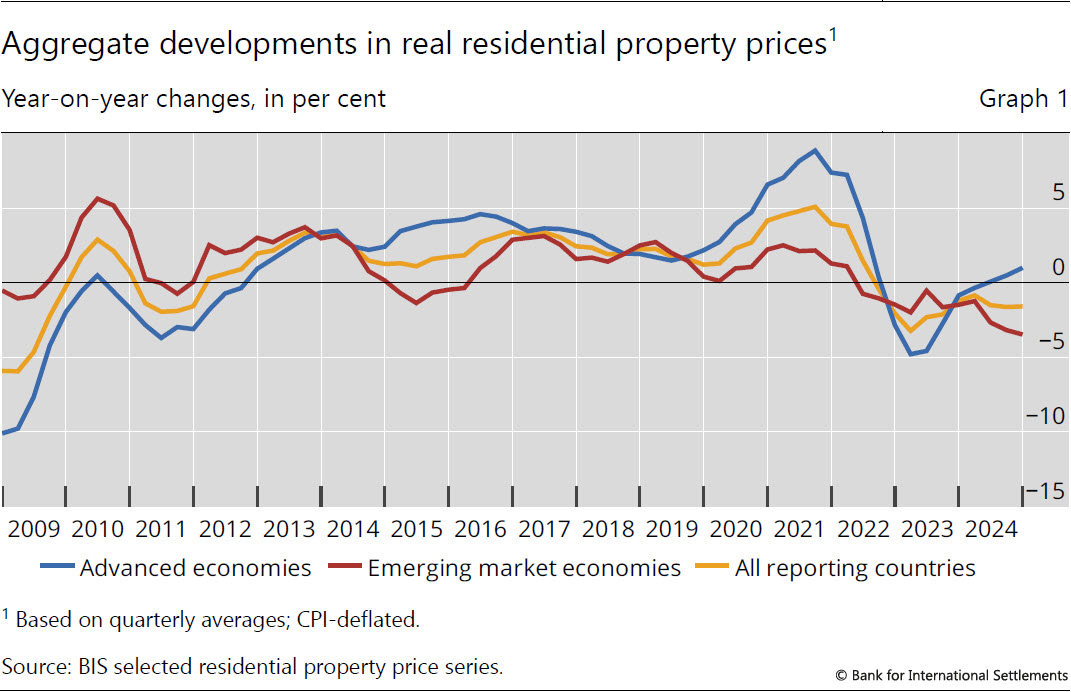

In the fourth quarter of 2024, global house prices deflated by consumer prices fell by 1.6% yoy, a rate unchanged from the third quarter.1 AEs saw a modest recovery, with real house prices increasing by 1.0% yoy in aggregate, marking the strongest growth recorded since Q2 2022. The rebound was especially notable in the euro area (+1.9%) and other European countries (+1.4%) (Table 1).

In contrast, prices in EMEs extended their decline observed since Q2 2022, dropping by 3.5% yoy in real terms (Graph 1), particularly in emerging Asia (–5.7%). This was only partially offset by stronger developments in Latin America (+3.1%) and central and eastern Europe (+1.9%).

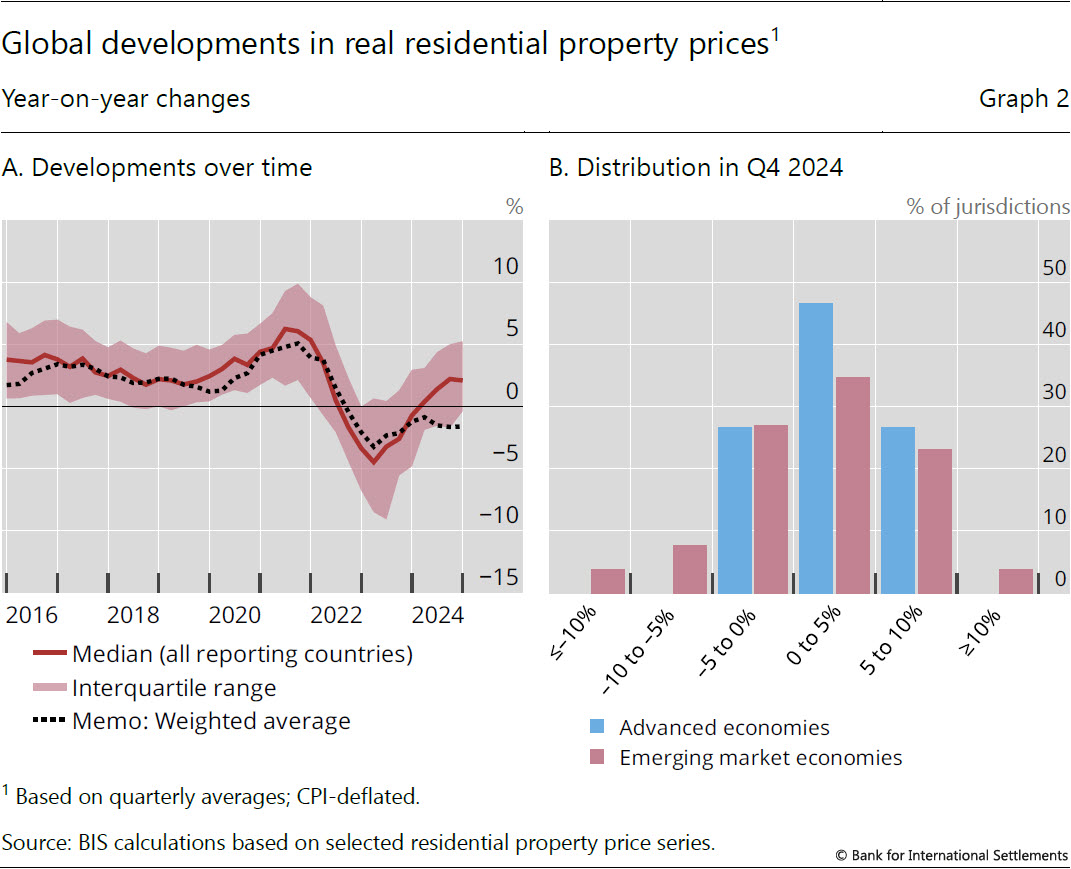

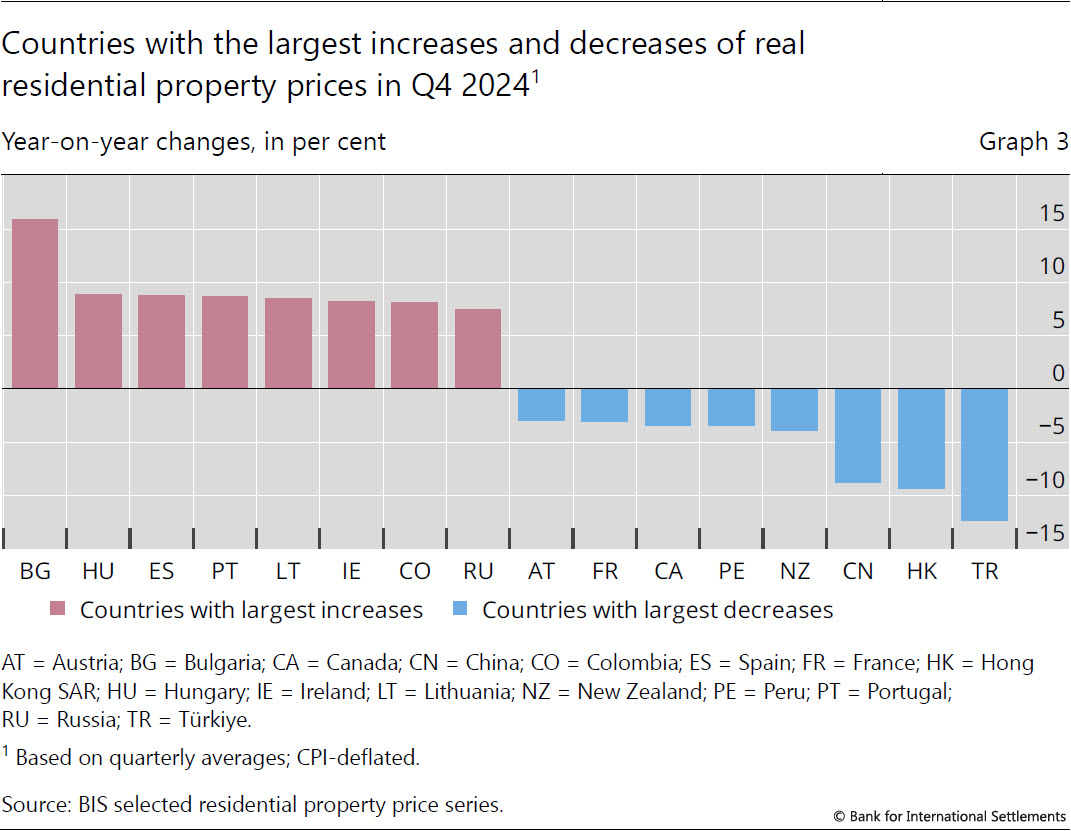

The fall observed in aggregate for global real residential property prices in Q4 2024 was mainly driven by a few large economies. In fact, the vast majority of jurisdictions experienced noticeable price increases, with the median price growth reaching 2.1% (Graph 2.A). About one half of AEs (45%) and one third of EMEs (35%) registered real price increases of 0 to 5%, and one fourth of AEs even saw robust growth in the 5 to 10% range (Graph 2.B).2 Among all reporting jurisdictions, Bulgaria registered the highest price increase (16%), followed by Hungary (9%) and Spain (9%). Conversely, prices fell significantly in Türkiye (–12%), Hong Kong SAR (–9%) and China (–9%) (Graph 3).

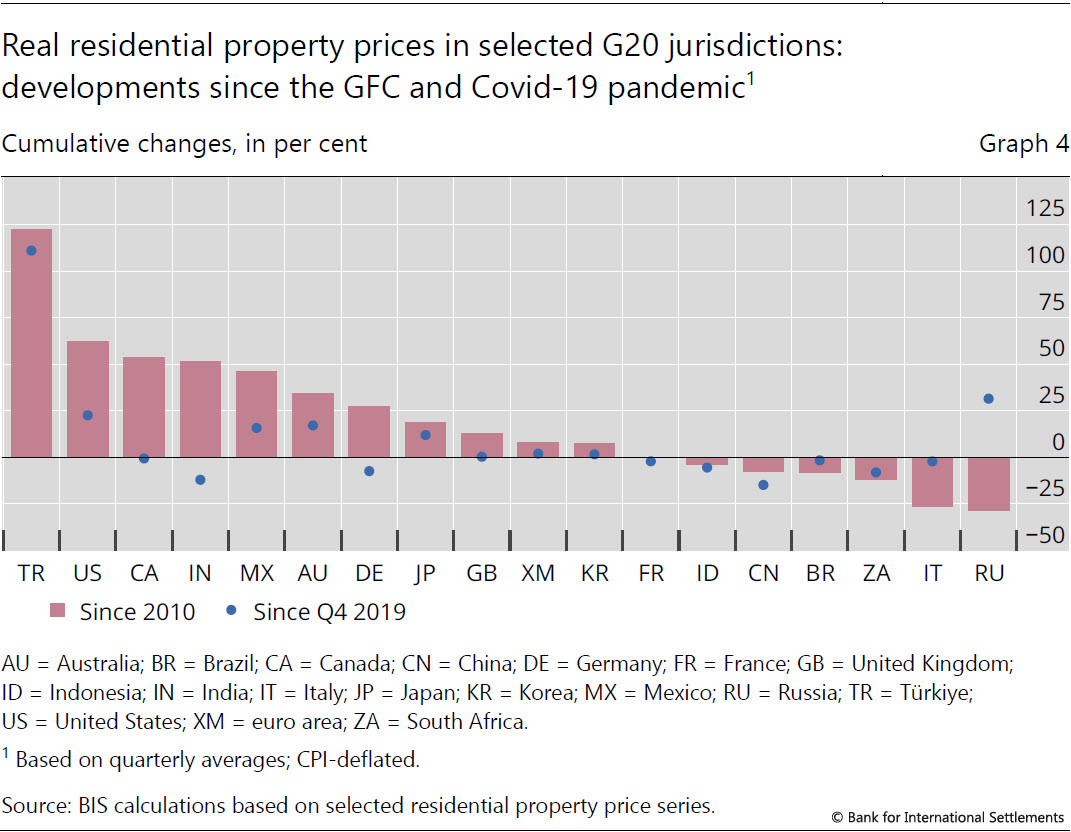

In most G20 economies, real house prices remain significantly above pre-pandemic levels, by 3% globally. However, there are significant differences between countries, with Türkiye leading (+111%) and China registering the steepest decline (–15%) since the pandemic.

From a longer-term perspective, aggregate real house prices exceed their post-Great Financial Crisis (GFC) levels by 20% globally (by 33% for AEs and 11% for EMEs). Since 2010, they have increased by more than 50% in non-European AEs, 22% in European AEs outside the euro area and 8% in the euro area. In EMEs, they increased by 20% in Latin America, 11% in central and eastern Europe and 10% in emerging Asia (Table 1). However, house prices remain below their post-GFC levels in one third of G20 jurisdictions, in particular South Africa (–12%) and Italy (–26%) (Graph 4).

Advanced economies

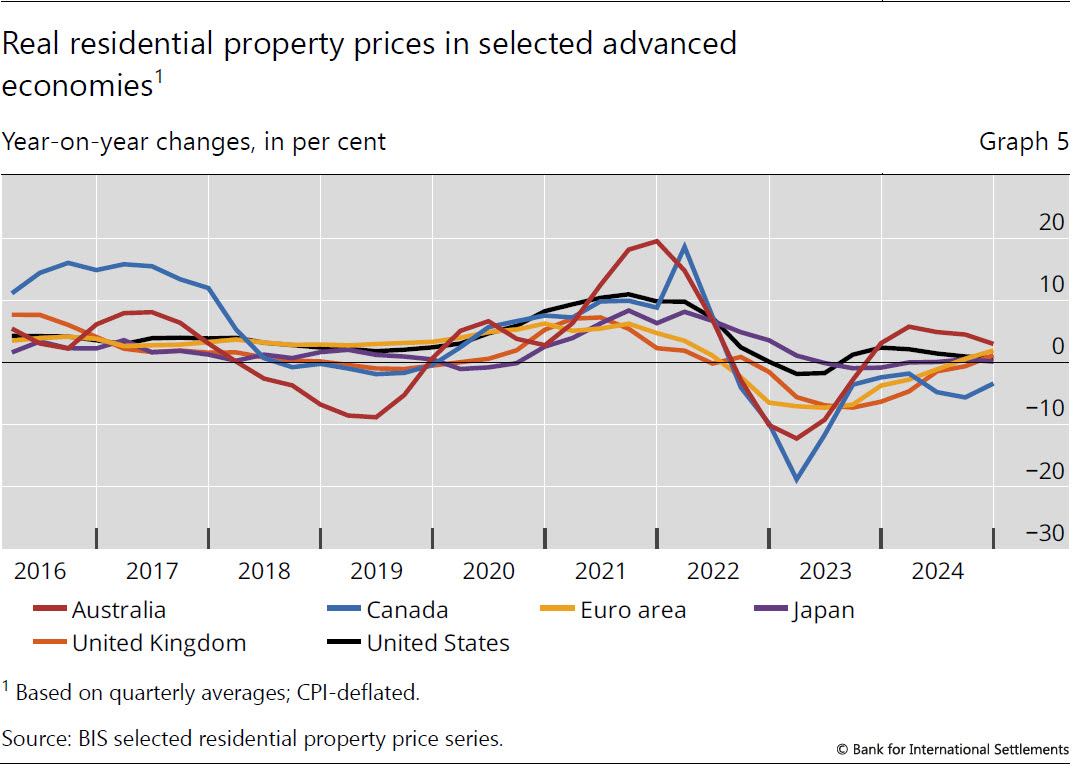

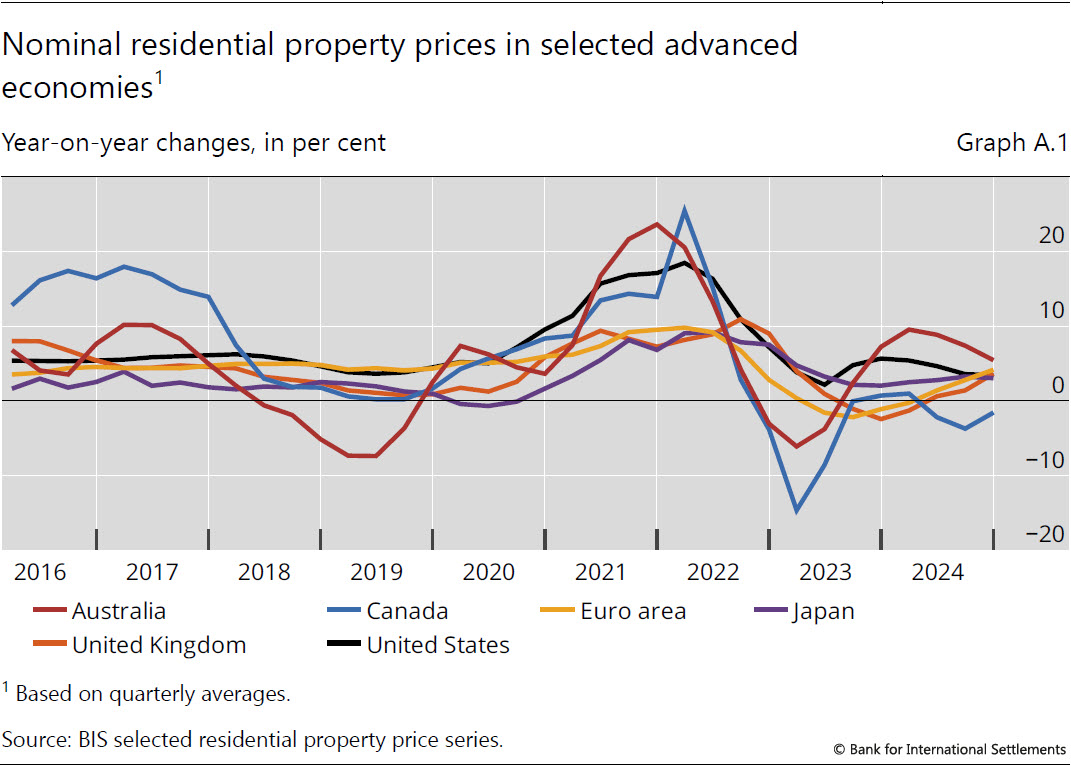

In aggregate for AEs, real residential property prices increased by 1.0% yoy in Q4 2024, the strongest growth since Q2 2022. Real house prices were up in the euro area (1.9%) and, for the first time since 2022, in the United Kingdom (1%). They remained broadly stable in the United States (1%) and Japan (0%) and continued to decline significantly in Canada (–3%) (Graph 5).

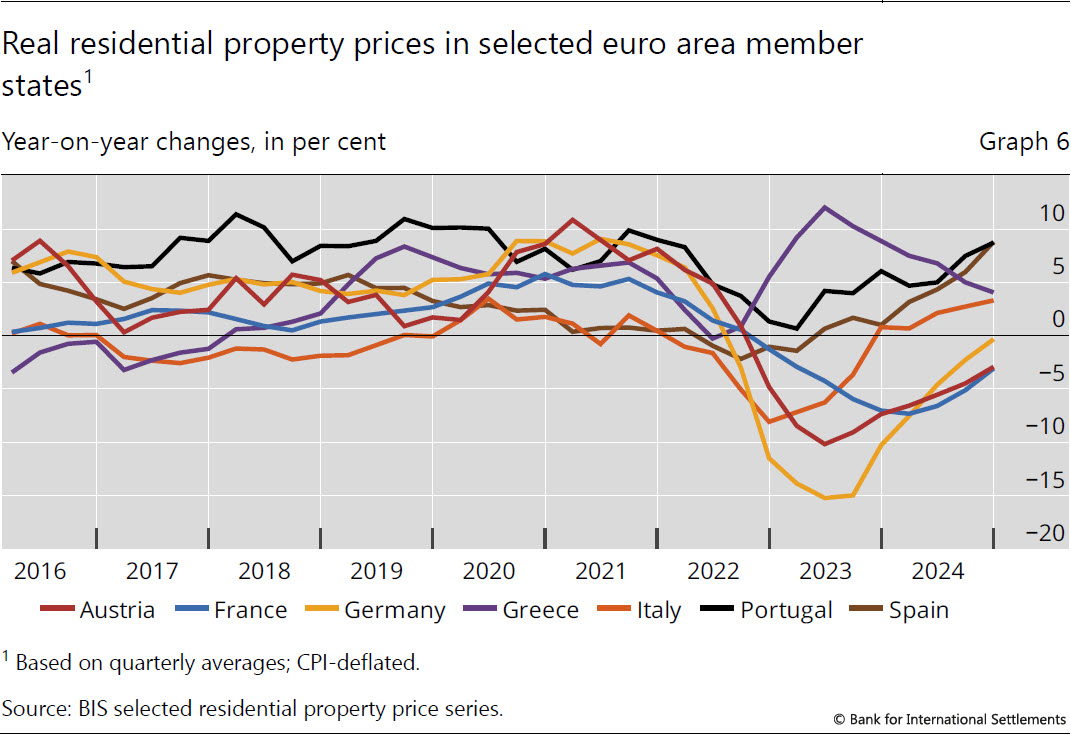

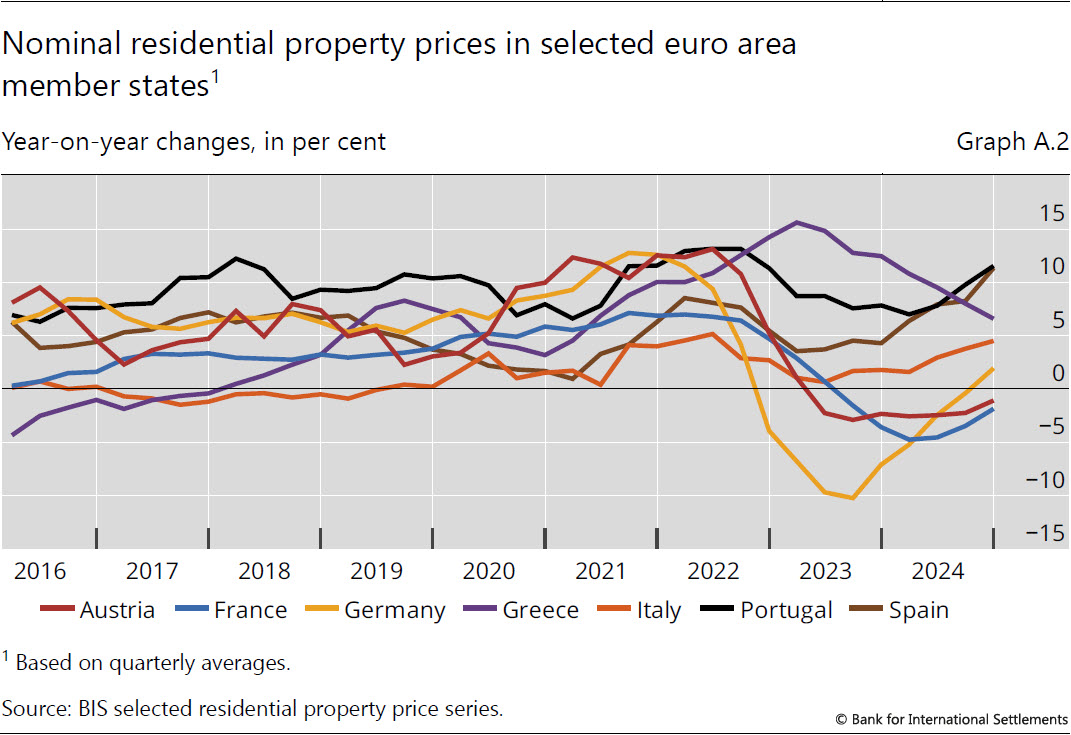

In Q4 2024, real house prices in the euro area increased by 1.9%. Spain (+9%) and Portugal (+9%) recorded the highest increases, followed by Greece (+4%) and Italy (+3%). Prices stabilised in Germany (0%) following an extended period of price declines. Meanwhile, they kept falling in Austria (–3%) and France (–3%), though at a slower pace than in previous quarters (Graph 6).

Emerging market economies

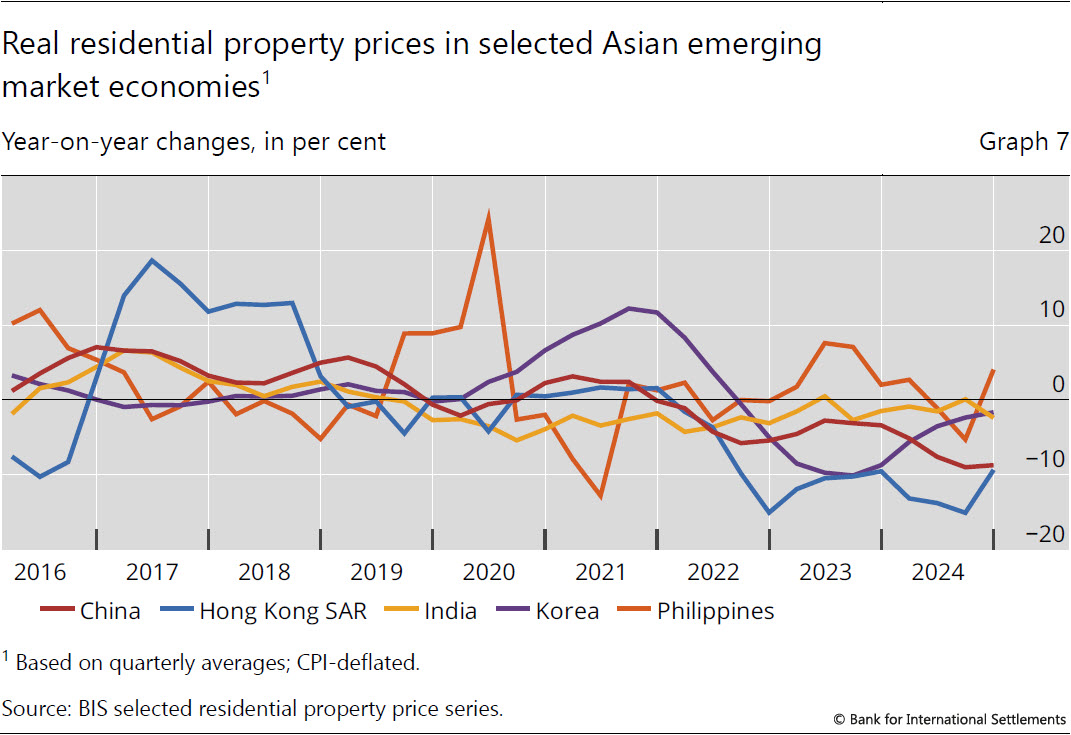

In Q4 2024, house prices in EMEs decreased further, by 3.5% yoy, largely driven by a few major Asian jurisdictions and despite the partial offset provided by Latin American economies.

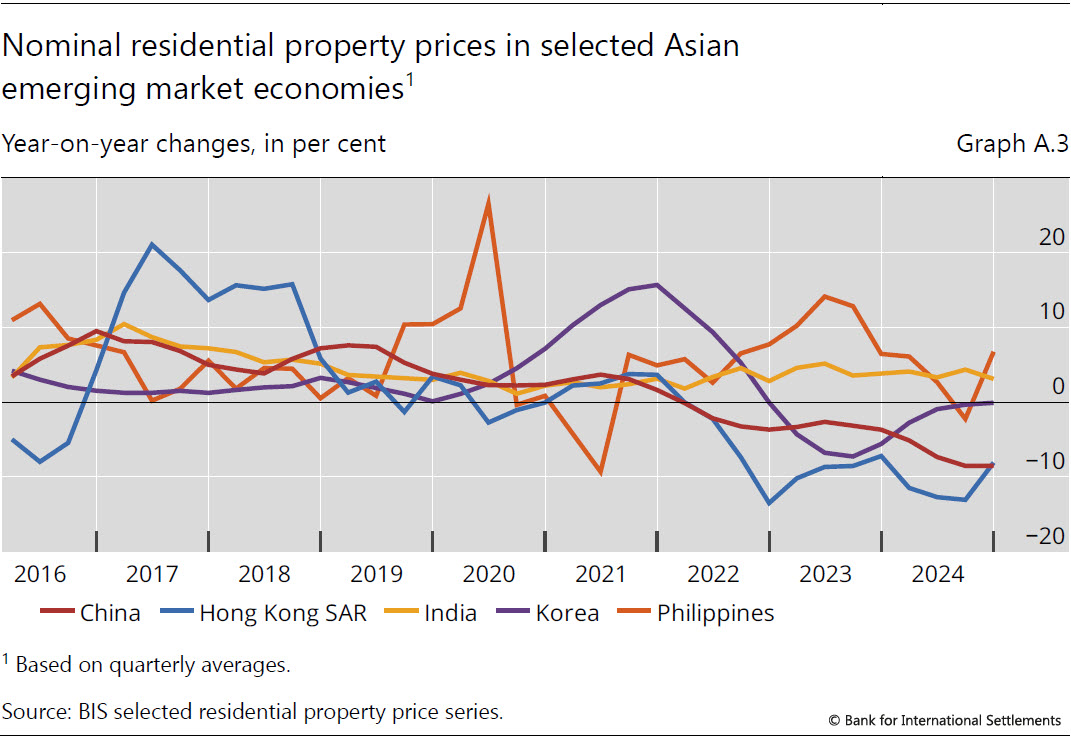

In emerging Asia, real residential property prices declined in many places: Hong Kong and China experienced significant declines of around 9% each. Prices also fell in India (–2%) and Korea (–2%). Conversely, prices rose in the Philippines (4%) (Graph 7).

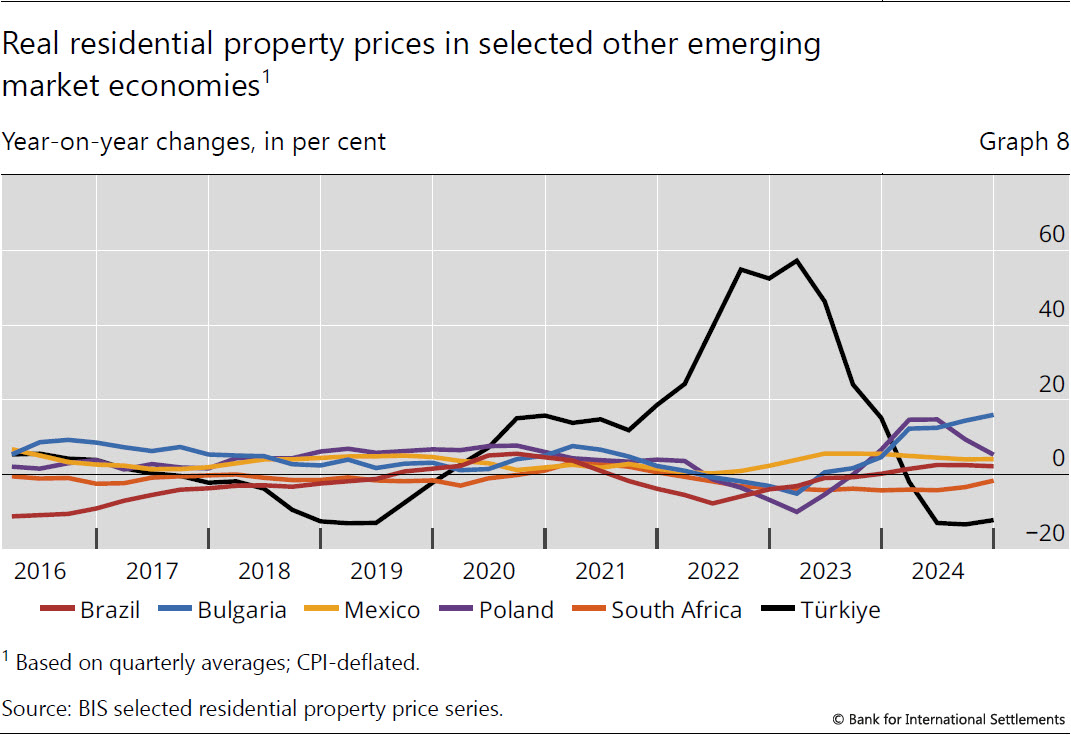

Real house prices in Latin America showed moderate growth, driven by Mexico (+4%) and Brazil (+2%). In central and eastern Europe, real prices rose by 1.9% in aggregate, with notable growth in Bulgaria (16%) and Poland (5%), while they fell in Türkiye (–12%). Prices continued to decline in South Africa (–2%) (Graph 8).

{kind=link}

{kind=link}