What does the data show?

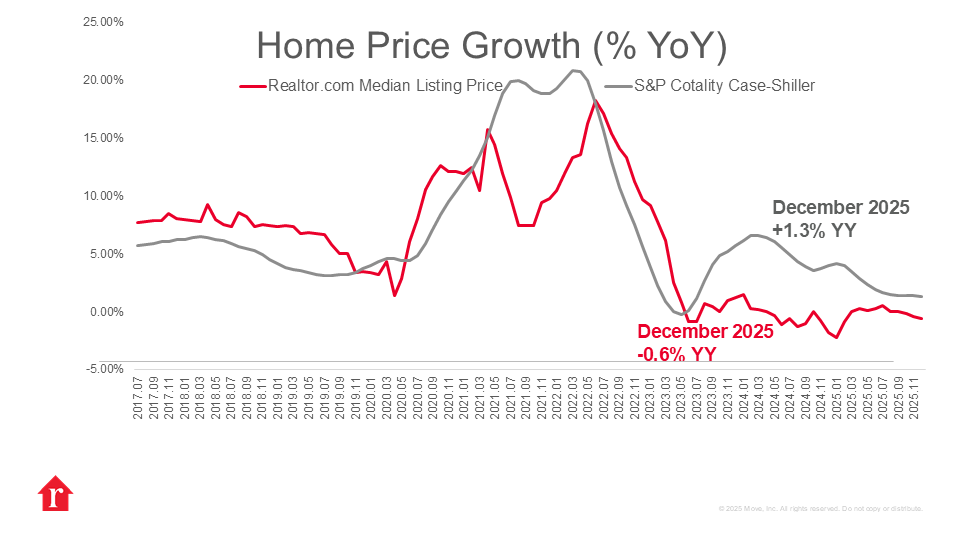

The S&P Cotality Case-Shiller Home Price Index showed national home price growth slowing through December, with the U.S. National Index rising 1.3% year over year, down slightly from 1.4% in November. At 1.3%, 2025 home price growth represents a clear downshift from the post-pandemic pace and underscores how affordability constraints and historically low turnover weighed on housing momentum throughout the year. December’s release reflects closings from October through December, a period when mortgage rates remained elevated before easing more recently.

Recent housing activity underscores that stabilization is occurring from a low base rather than signaling a broad rebound. Existing-home sales for 2025 totaled just 4.063 million, the lowest annual level since 1995, reflecting the persistence of rate lock-in. At the same time, national inventory has more than doubled since early 2022, yet price levels have remained resilient. Longer days on the market and elevated delistings, rather than widespread price capitulation, explain much of this resilience. Sellers, in many cases, appear more willing to withdraw listings than materially reset pricing expectations, keeping supply from exerting stronger downward pressure.

How did trends vary by region?

Regional divergence widened meaningfully. Midwest and Northeast metros led performance, with Chicago (+5.3%) and New York City (+5.1%) posting the strongest annual gains among the 20 tracked cities, followed by Cleveland (+4%). These markets continue to benefit from tighter resale inventory and more constrained new supply. By contrast, several Sun Belt metros extended their corrections, with Tampa (-2.9%), Denver (-2.1%), Phoenix (-1.5%), Dallas (-1.5%), and Miami (-1.5%) finishing the year in negative territory. Markets that experienced outsized pandemic-era appreciation are now seeing more persistent normalization as inventory rebuilds and demand remains payment-sensitive.

On a monthly basis, the data was mixed. Before seasonal adjustment, the national index declined 0.3% in December. After seasonal adjustment, prices rose 0.4%, suggesting that while year-over-year growth has cooled substantially, underlying price levels are not collapsing but instead adjusting gradually.

What is ahead for housing?

Broader economic conditions are beginning to tilt modestly in housing’s favor, though durability remains the key question. A softer inflation backdrop has helped pull mortgage rates down to their lowest level since 2022, improving purchasing power just ahead of the spring season. Real income growth is benefiting from easing price pressures and steady wage gains, offering some relief after several years of strained affordability. However, nearly five years of elevated home prices have partly offset those income gains and continue to weigh on consumer confidence. A sustained stretch of lower inflation and a more certain labor market will be necessary to rebuild confidence and translate improved rate conditions into a durable housing rebound.

Looking ahead, the path for home prices will depend heavily on spring supply dynamics. A sustainable housing recovery requires both renewed buyer demand and a meaningful increase in fresh listings. Without a material easing of the lock-in effect, lower mortgage rates risk reigniting competition in already supply-constrained markets, potentially sustaining price growth. As a result, national home price appreciation is likely to persist, though at a tempered pace and increasingly shaped by local inventory conditions rather than broad macro momentum.

{kind=link}