Last week’s data tracked a shifting economic trajectory over the last several months. While the latest reading on first-quarter GDP confirms the economy started the year with steady growth, subsequent inflation metrics from April moved higher, heavily influenced by global geopolitical pressures. This persistent pricing pressure has started to weigh on consumer sentiment, triggering a recent dip in overall confidence. Meanwhile, markets have maintained momentum, even as the latest data solidifies expectations that the Federal Reserve will hold monetary policy steady for the foreseeable future.

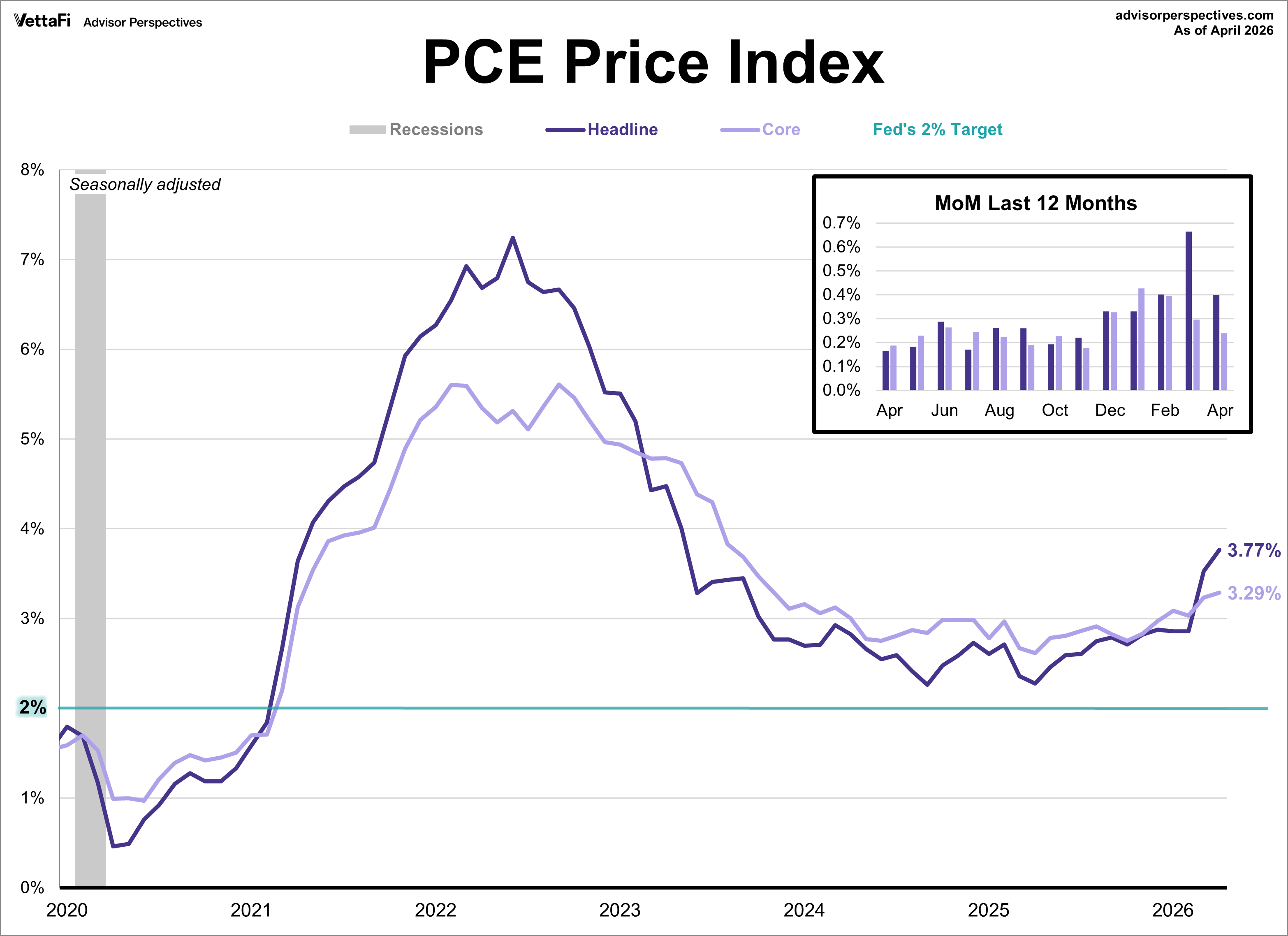

Inflation Pressures Intensify

Ongoing conflict in the Middle East continued to drive up energy costs, pushing the Federal Reserve’s preferred inflation gauges to multi-year highs in April. The headline PCE index rose 3.8% annually, its highest level since May 2023, and was up 0.4% from the previous month. Meanwhile, core PCE (which excludes food and energy) rose a more modest 0.2% on a monthly basis, but still reached a 3.3% year-over-year clip, marking its highest level since late 2023. Both annual figures matched expectations and both monthly figures were slightly lower than forecasted, however, the impact of the war remains evident across recent inflation reports with price pressures likely to persist in the coming months.

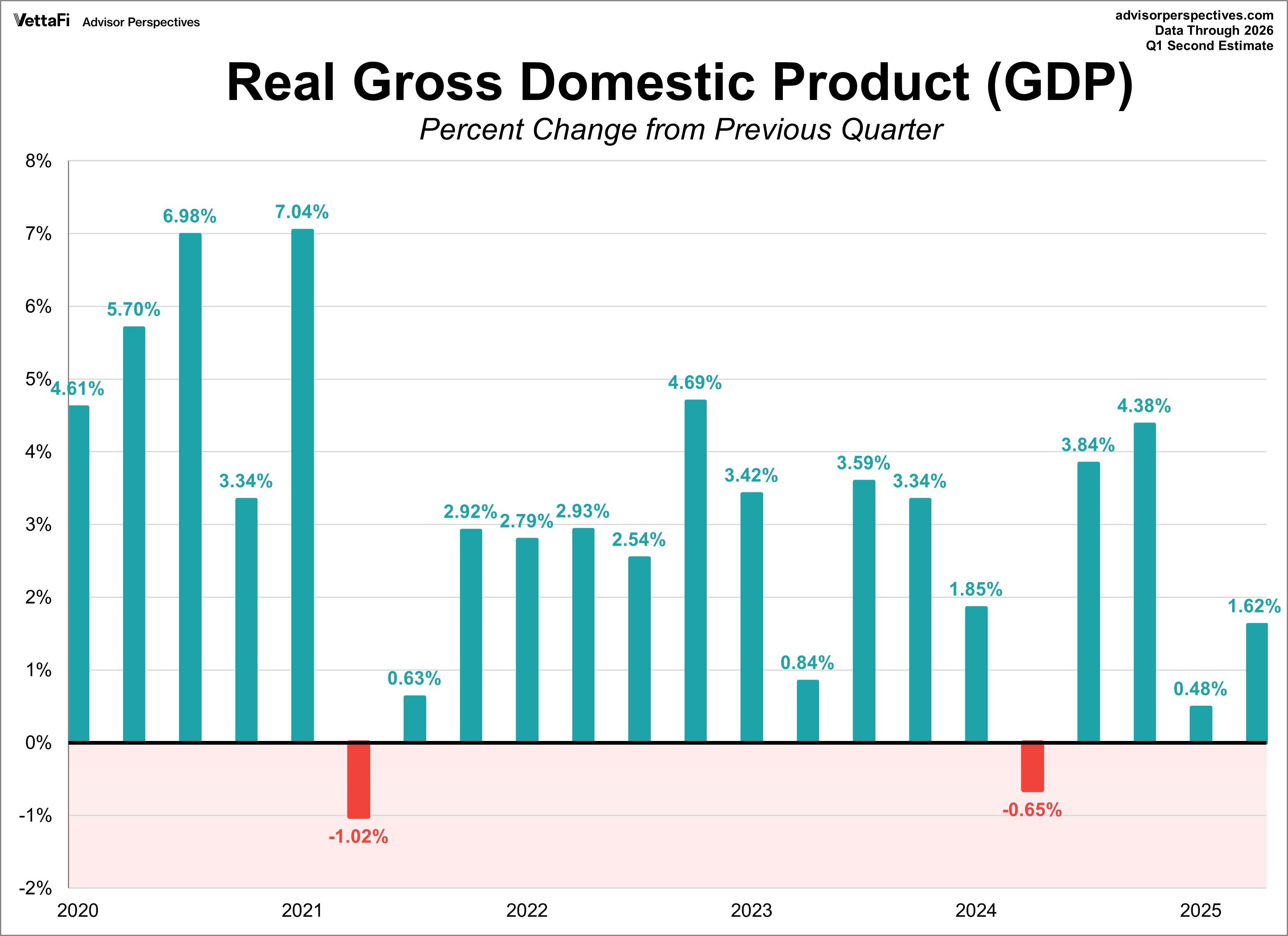

Economic Growth Slower Than Expected

The U.S. economy grew at a steady pace at the start of 2026, though less than initially expected. According to the BEA’s second Q1 estimate, real GDP expanded at a 1.6% annualized rate, a marked improvement over the 0.5% growth recorded in the final quarter of last year, though it remained below the projected 2.0% forecast. Growth during this period was largely fueled by an increase in exports, business investment, consumer activity, and government spending.

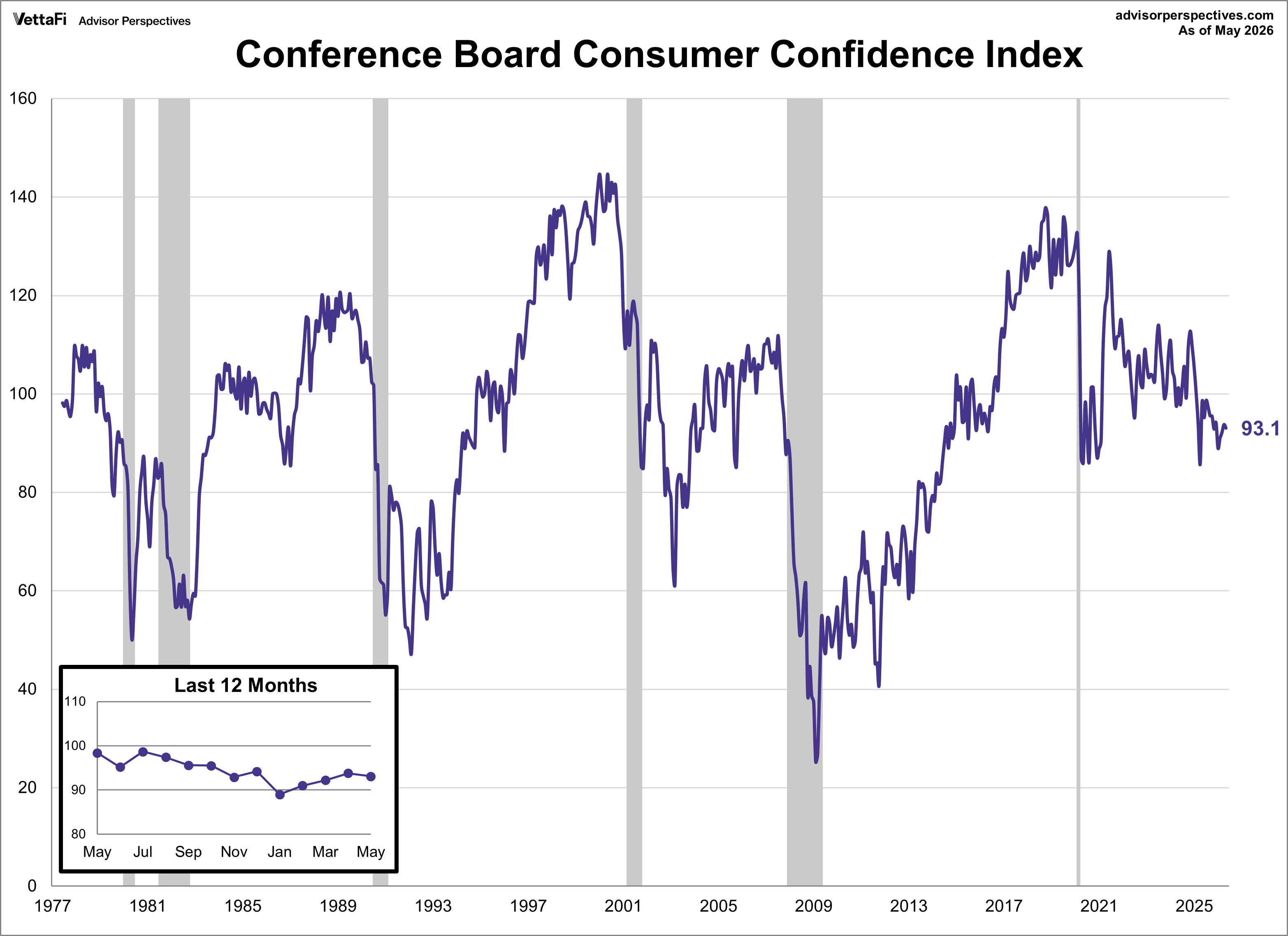

Consumer Confidence Dips on Inflationary Fears

Consumer confidence fell for the first time in four months in May, driven by growing concerns over the inflationary impact of the Middle East conflict. The Conference Board Consumer Confidence Index® slid 0.7 points to 93.1, though it remained above the forecasted 91.9 level.

While improved expectations for the business and labor markets provided some support, the index was primarily dragged down by weakening perceptions of current conditions. Furthermore, persistent mentions of geopolitical strife and high prices from consumers underscore their concerns about how the war is affecting their wallets.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer confidence.

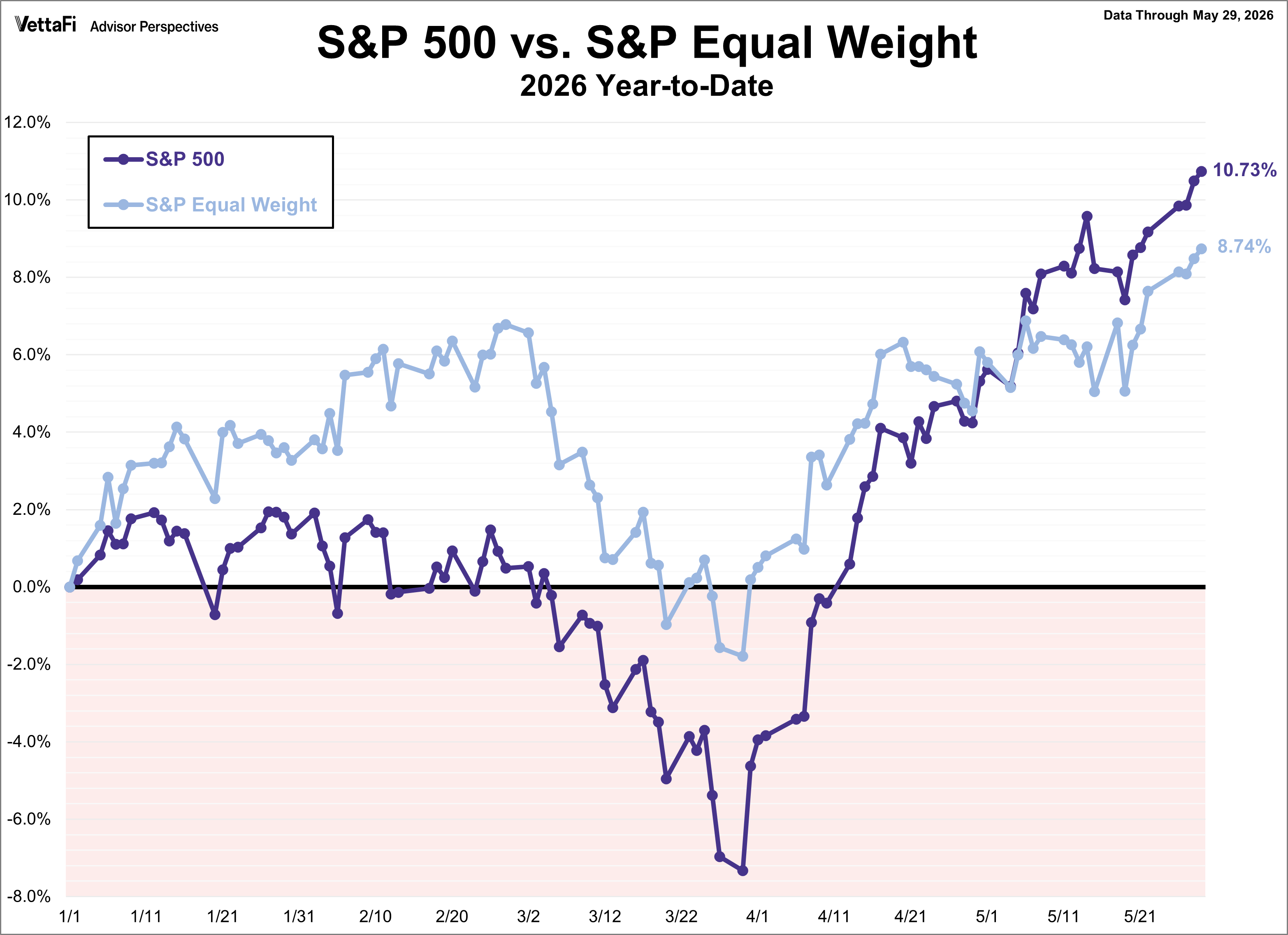

Market Reactions

Building on the previous week’s strength, the S&P 500 rose every day last week and set multiple new record highs. With a 1.6% weekly increase, the index secured its ninth straight weekly gain, matching its longest winning streak from 2023. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 1.5% last week. Meanwhile, the S&P Equal Weight Index was up 1.0% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 1.1%.

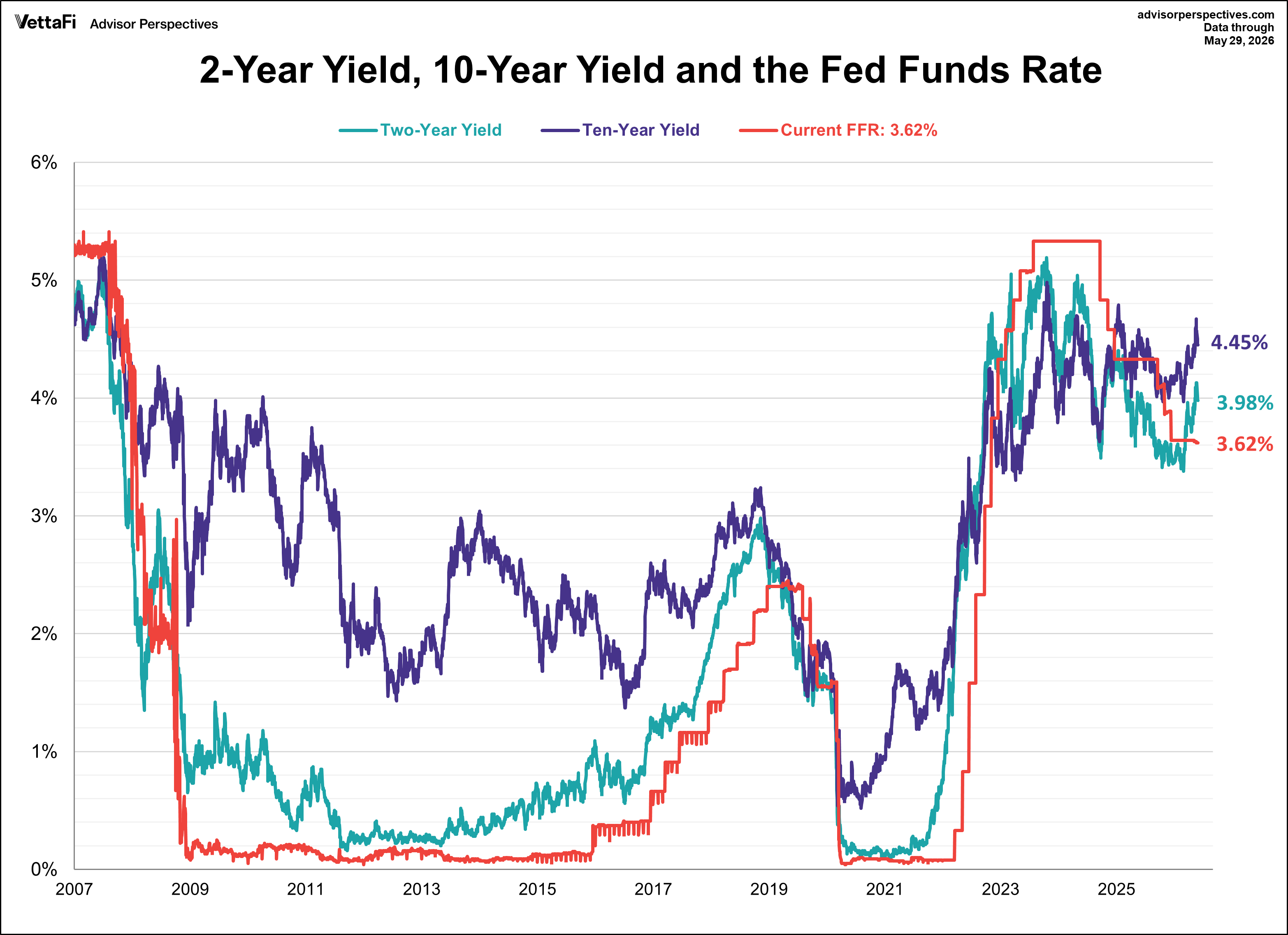

The 10-year Treasury yield finished the week at 4.45%, while the 2-year note finished at 3.98%.

The CME FedWatch Tool currently shows a 99% likelihood that the Federal Reserve will hold rates steady at its June meeting, with just a 1% chance of a cut. Markets are currently pricing in a 25 basis point hike by the beginning of 2027 followed by a pause through the remainder of the year.

Looking Ahead: Economic Data for the Week of June 1, 2026

- Monday: S&P Global Manufacturing PMI (May), ISM Manufacturing PMI (May)

- Tuesday: JOLTS Job Openings (Apr)

- Wednesday: S&P Global Services PMI (May), ISM Services PMI (May), ADP Employment Report (May)

- Thursday: Weekly Jobless Claims

- Friday: BLS Employment Report (Apr)

Originally published on Advisor Perspectives

For more news, information, and strategy, visit ETF Trends.

{kind=link}